February 4, 2022

Please find our 2021 annual letter below. We provide an update on our enhanced strategy, Vanshap 2.0, discuss our attempts to hunt the ‘next Amazon,’ and provide a brief overview of our investments. We welcome your feedback.

*****

Update on Vanshap 2.0

During the summer of 2020, after the dramatic COVID-19-led correction in the equity markets, we performed a full-scale re-evaluation of our investment strategy. The evolution was briefly discussed in a portfolio update piece entitled Vanshap 2.0 and at our 2020 Annual Partners’ Meeting. To summarize, the most significant improvements we undertook were:

- Heightened emphasis on managerial talent, taking advantage of hidden value-creation optionality difficult to detect in quantitative screening.

- Greater focus on quality businesses with long-term reinvestment opportunities at attractive rates, while decreasing our portfolio turnover.

- Increased use of industry sources to obtain more detailed perspective on competitive dynamics.

We remain focused on less efficient international markets and highly disciplined regarding valuations. Exceptionally well-managed companies with sustainable growth dynamics are hard to find at attractive prices. In recognition of this fact, we heavily concentrate our portfolio in the top five investments and extend our already long-term investment horizon. Having exceptionally strong support from our founding partner Markel Corporation and a truly long-term oriented partner base, allows us to take this highly concentrated, durable approach.

Analyzing our own historical returns suggests that our highest conviction investments materially outperformed our smaller holdings, contributing significantly more to overall returns. While we understand higher concentration invariably increases volatility, we are certain that this is the only way fundamentally oriented investors can generate strong results over the long term.

We have also recognized that while our strategy represents the majority of our personal portfolio, Vanshap typically only represents a minority for many of our investors. Therefore, a highly concentrated portfolio prevents over diversification from our partners’ standpoint. Relatedly, we are mindful of holding too much cash for the same reason and recognize the enormous opportunity cost.

The end result of incorporating these changes has been a focus on larger and far more liquid securities – leading to an upward drift in portfolio median market capitalization. Please note our investments will not be of the U.S. blue-chip variety and our strategy will largely remain market capitalization agnostic. Improved liquidity will allow us considerable flexibility to reposition the portfolio when needed.

Our enhanced strategy didn’t come about haphazardly. Instead, we have been deliberately learning, working to understand the power of buying a business with a huge opportunity for profitable capital deployment opportunities ahead. Having a longer potential growth runway frequently coincides with having to pay higher multiples, and we must allow ourselves leeway to pay for superior, scalable business models. However, multiples can become far too high, as we have seen over the past two years. Given our experience of living through the markets of the Technology Bubble and Great Financial Crisis, we had been reticent to open our mind to higher multiple companies, which was been to our detriment. Going forward we intend to walk the narrow path of investing in attractive growing companies while not paying exorbitant prices for them—a feat easier said than done in recent years—but a path we are determined to take.

While the ultimate verdict of Vanshap 2.0 remains to be seen, we are confident that the results over a multi-year period will prove superior.

*****

Chasing the Next Amazon

As part of our self-reflection and evolution, we have been analyzing exceptionally well-managed companies with strong competitive moats and the ability to reinvest capital over long periods of time at attractive rates of return. Ideally, investing in these businesses would allow us to step off the endless idea treadmill, reducing the need to constantly recycle portfolio holdings. Of course, we must remain valuation disciplined.

We admittedly underestimated the power of scalable businesses with strong network effects, particularly those that are heavily reinvesting in operations and thereby producing accounting losses. We have recognized these businesses can eventually become massively profitable after enough customers are addicted, creating operating leverage and upselling opportunities. Amazon is perhaps the quintessential example.

While others have a far more in-depth understanding of Amazon’s history, we believe an often-overlooked factor that led to the group’s success was the lack of strong competition. Indeed, Amazon was relatively unchallenged in online retailing and delivery for an extended period from the early to mid-2000s. Obviously, the competition was caught off guard, passing up one of the best opportunities over the past decade, investing in a dominant, scalable e-commerce platform in the world’s largest retail market. Mea culpas are due.

Many investors, including ourselves, are making up for lost time and are now trying to find the ‘next Amazon.’ Candidates that we have begun to analyze are Alibaba in China, Coupang in South Korea, Mercado Libre in Brazil, Ozon in Russia, and Sea in Southeast Asia, to name a few. We have yet to make an investment in these businesses for a variety of different reasons, but primarily because of competition and valuation.

Given a confluence of sector performance chasing, cheap capital, and COVID-19 accelerating e-commerce trends, many of these stocks caught fire with valuations soaring to stratospheric levels early in 2021, as we gradually started to accelerate our work. Rather than immediately jumping on the band wagon, we took a step back and fundamentally tried to understand these business models. Are they as good as everyone thinks or is Amazon a special case that is hard to replicate? Thus far, we believe that many of these businesses are too easily being given the benefit of the doubt and that investors are failing to see the differences in Amazon’s environment versus today’s highly competitive landscape.

Aside from the undeniable brilliance of Jeff Bezos and the strong execution of the management team, many additional factors contributed to Amazon’s success. By far the most important being a lack of strong competition, in our opinion. We believe these three factors previously constrained competition, but are no longer present.

-

Poor mobile data usage. Mobile data usage is growing dramatically in both the developed and emerging markets, a well-known trend that many are attempting to exploit. This is leading to nearly all sizable retailers creating an online e-commerce and logistics strategy, likely to dilute the ultimate market share of the giants and lead to category leakage, such as furnishings or luxury goods. Perhaps more important, rapidly expanding 3G/4G infrastructure has provided a viable avenue for social media and video content to proliferate, with extremely promising 5G technology on the horizon. This is creating other venues to buy merchandise (both directly and indirectly) that didn’t exist for a younger Amazon, likely to result in further dilution of retail market share and even more importantly, marketing dollars.

-

Lack of access to cheap capital. Ultra-low interest rates and robust private equity markets are providing a long operational runway for industry newcomers with little need for near-to-mid-term profitability. Additionally, strategic behemoths like Alibaba are looking globally to plow capital into potentially competing platforms to ‘hedge their bets’ against aggressive local market upstarts.

- Not understanding loss leader business model. Perhaps the hardest item to quantify is the previous incomprehension of the loss-leader business model. The concept has been omnipresent, but was temporarily forgotten as the digital world took shape and retailers didn’t realize that logistics itself could be a loss leader. Amazon was essentially providing a service of convenience, logistics, at a very low profit margin with high capital intensity to ‘eat’ market share and sell higher value services, which we now see with Prime, video content, advertising, cloud, etc. This business model is now fully understood as almost all the new e-commerce platforms are attempting to add tangential product offerings. These new companies are accepting large logistics-led operating losses in the near-to-mid-term with hopes that operational leverage and upselling opportunities accelerate over the longer term.

We believe there are too many deep-pocketed players trying to emulate Amazon, which could suppress margins for an extended period of time until a ‘shake out’ of weaker competitors is accomplished.

For instance, the Latin American market has numerous well-capitalized, savvy players such as Amazon, Americanas, Mercado Libre, and now Sea-owned Shopee. How long until pricing power and a clear market share leader emerge? Investors may be underestimating the time required to achieve reasonable margins and the difficulty in building more attractive business lines, as peers and other fintech players compete for the same share of wallet.

We are not only looking for high quality scalable e-commerce, data, or content, but also a business not valued as though a winner-take-most result is guaranteed. Just because one may correctly pick the eventual industry winner, assuming there even is only one, doesn’t mean the path to strong capital returns will be smooth. If these risks are not appropriately incorporated into the valuation, we believe further share price declines like what has occurred over recent months are likely as profitability continues to be elusive.

Even Amazon, the clear U.S. winner which emerged with the highest take-rates in the world, may have been far less successful without the high margin Amazon Web Services (AWS) unit. Leading sell-side analysts estimate AWS may be worth nearly half the current value of the company, meaning cumulative investor returns could have theoretically been cut in half, resulting in a 9% per year lower annualized return over the past decade. Despite Amazon’s near single-handed domination of e-commerce in the U.S. and enviable take-rates, much of Amazon’s legendary share price returns may have actually been tied to a business unit that few if any other global e-commerce players will be able to replicate.

Additionally, we should note that 10 years ago e-commerce as a percentage of total retail sales was ~5% in the U.S. similar to the penetration in Latin America or Southeast Asia today. Yet, the forward price-to-sales multiple investors were paying for Amazon at the time was only ~1.3x, compared with the current valuation of ~6.0x for regional leaders Sea and Mercado Libre. While Amazon has undoubtedly added numerous highly attractive business segments, we continue to believe valuation plays a significant role in determining investment success.

Finding a clear industry winner at a reasonable price is exceptionally difficult. In Kaspi, we have found the undisputed e-commerce, payments, and consumer loan winner in Kazakhstan which could soon dominate the region, but admittedly has a smaller total addressable market. We hope to add another e-commerce platform to the portfolio valuation dependent. The hunt continues!

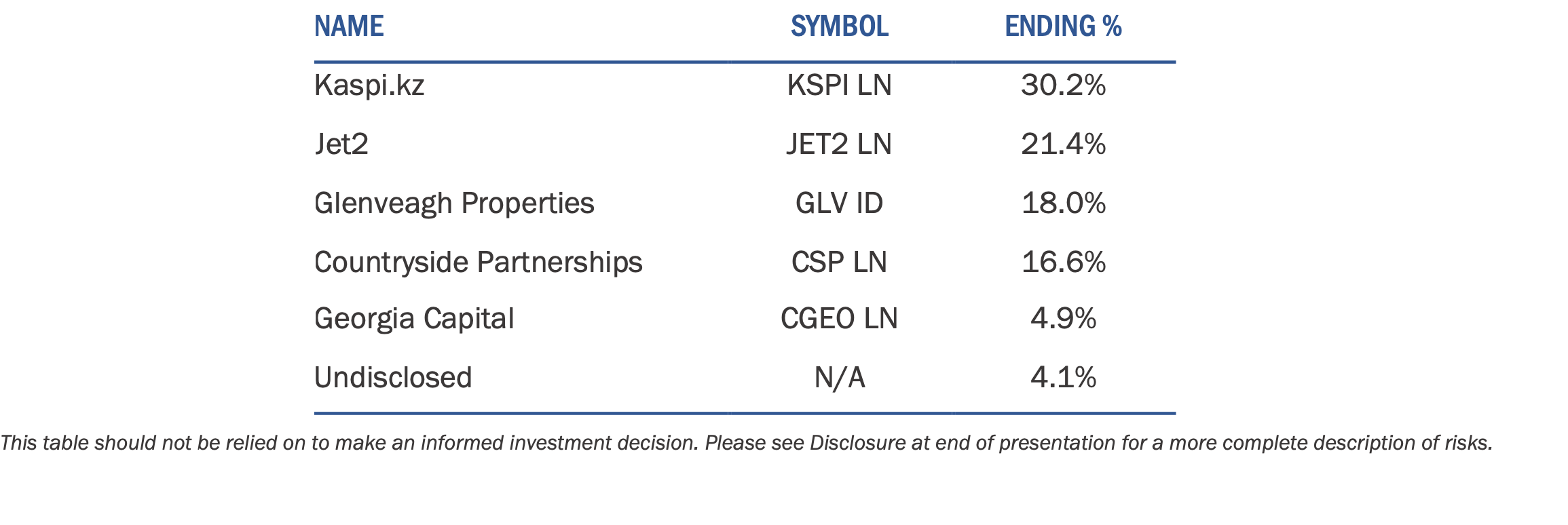

Vanshap Capital Positions at December 31, 2021

Please find our brief portfolio updates below. We have only included brief summaries, so please let us know if you would like additional detail. As you can imagine, we have a lot to add.

Please find our brief portfolio updates below. We have only included brief summaries, so please let us know if you would like additional detail. As you can imagine, we have a lot to add.

Kaspi.kz (LON: KSPI)

Description: Largest consumer financial services and e-commerce platform in Kazakhstan.

Thesis: Highly dynamic, dominant fintech trading at ~12x earnings with local and regional market penetration opportunities and years of +20% earnings growth likely ahead.

Update: Deepening e-commerce product offering, and growing user engagement coupled with lack of competition is leading to better-than-expected growth. Taking initial steps to expand payments and select lending products in Ukraine. Evidence of successful new services adoption such as digital government programs, SME lending, and travel further entrenches users. Potential future product offerings such as food delivery and classifieds are in the pipeline. Market continues to underestimate the power of the ecosystem, with exceptional growth potential for years to come. Violent local demonstrations that occurred during January 2022 have ceased and economic stability has returned.

Jet2 (LON: JET2)

Description: Rapidly growing, largest sun destination packaged holiday operator in the U.K.

Thesis: Best managed company in the industry with significant brand and customer loyalty advantage, trading at ~8x recovery earnings, with double-digit multi-year growth runway ahead as market share earned from weaker competitors.

Update: Company reports demand for summer ’22 bookings is now at pre-pandemic levels, and regulators may tighten customer cash rules which will negatively impact weaker competitors. Jet2 has recently announced a large fleet renewal/growth plan with firm and option orders up to 75 Airbus 321Neos, expected to drive significant cost efficiencies over time.

Glenveagh Properties (ID: GLV)

Description: Largest residential developer in Ireland, expanding in capital constrained affordable segment.

Thesis: Unleveraged, well-managed builder standardizing best practices resulting in construction efficiency trading at ~9x mature run rate earnings multiple, with goals of increasing capital efficiency and returning excess capital to shareholders.

Update: Home demand remains robust. Government significantly expanded first-time home buyer assistance program to include up to 30% equity support in certain cases. Local housing authorities moving forward with affordable public/private partnerships to stimulate supply, as evidenced by company’s recent preferred bidder announcement and other projects reportedly in the works. Institutional demand for urban apartments has fully recovered allowing company to forward-sell several large remaining projects, accelerating the progression to a more capital efficient, affordable housing business model. Labor shortages and wage pressures remain an ongoing concern with the company accelerating manufactured solutions in response.

Countryside Properties (LON: CSP)

Description: Largest affordable housing developer in the U.K. with unique capital-lite business model.

Thesis: Rapidly becoming a capital-lite, less cyclical developer with sole focus now on Partnerships segment. Group should command a materially higher market multiple as business scales and capital is aggressively returned to shareholders. Shares trading at only ~7x stabilized earnings multiple assuming return of excess capital via share repurchases.

Update: Formally announced wind down of capital-intensive Housebuilding division along with expansion of Partnerships into the southeast region, while targeting a return of £450 million to shareholders via repurchases. Company has announced target to generate capital returns of +40% on a ~£750 million asset base by FY ’24. New Chairman/CEO along with U.S. shareholder base are now actively engaged to ensure capital efficiency and proper operational execution, which is now in question following disappointing 2021 results. Cost pressures around wages and industry-wide exterior cladding liabilities continue to weigh on sentiment. We remain cautiously positive on our thesis, albeit unit growth execution may be more challenging than first believed.

Georgia Capital (LON: CGEO)

Description: Holding company of market leading Georgian businesses.

Thesis: Dominant businesses in mostly non-cyclical industries trading at +45% discount to our estimate of recovery NAV, with management strongly in favor of discounted share repurchases.

Update: Discord between Georgian political factions are a concern, but all sides remain committed to a pro-business, pro-western path for the country with some common ground recently reached. Company is making strategic progress with continued expansion in education, buyout of minority’s share of pharmacy business, and disposal of the large asset-intensive water utility asset. Proceeds will be used to deleverage the balance sheet, buy back shares, and make strategic acquisitions. Market eyeing NATO discussions with Russia to gauge regional political risk. We have reduced our holding due to our previously mentioned strategy shift to focus on more liquid investments, with greater long-term growth and capital reinvestment potential.

Thank you once again for your continued support, we greatly appreciate your trust.